Once upon a time there were three little pigs, and, although they were brothers and looked a lot a like, they could not have been more different.

The first little pig was hard-working and thrifty. He spent very little of his income, saving and investing as much money as he could. He lived with his mother well into adulthood, helping her with her expenses. He finally bought a home of his own when he could afford to pay for it all in cash. As you might expect, the thrifty little pig’s home wasn’t flashy, but it was all his, free and clear.

The second little pig didn’t save very much of his income, but he earned a lot of money as a rising executive, and he had an uncanny luck in the housing market. He bought a condominium on his 18th birthday, then traded up to his first single-family home before he was 21. By the time he was 30, the lucky little pig owned a very stately executive home — and he had been able to make a whopping 50% down-payment.

The third little pig wasn’t very good at working hard, and he had never kept a job long enough to get a raise. He wasn’t at all good at saving money, but he could borrow and spend it better than any little pig anywhere. Like the lucky little pig, he moved away from home early, but he just kept moving — from apartments to friends’ couches to rental homes and then to one girlfriend’s house after another.

If you are a liberal, you may be thinking of the third brother as the unfortunate little pig. If you are a conservative, you will want to call him the lazy little pig — or worse. To keep the peace, let’s just call him the puerile little pig — the little brother who never quite grew up.

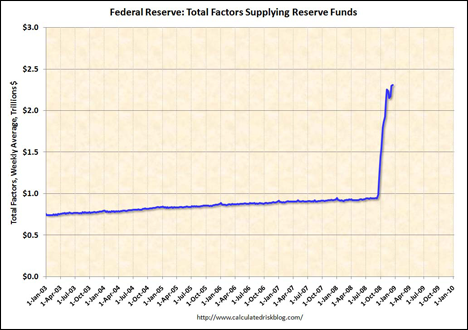

The original version of this story was about construction quality as a metaphor for planning ahead, anticipating disasters so they don’t take you by surprise. But the world of real estate has changed a lot since then. The most important Read more