by Brian Brady

Commercial Real Estate Finance Expert

Structured Debt and Equity

Licensed Real Estate Broker in AL, CA, and FL

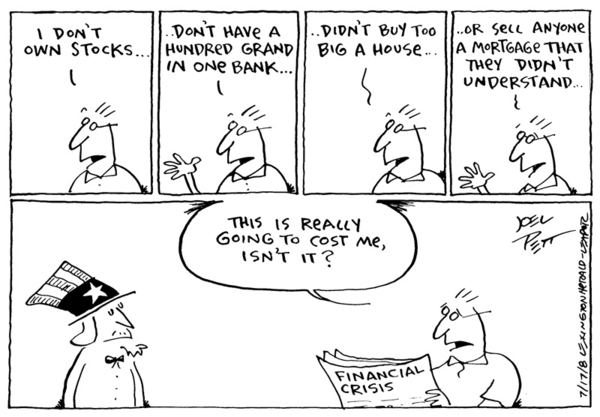

I guess we saw this coming. Robert Kerr has been talking about the collapse of the GSE’s, in the comments section on Bloodhound Blog, for close to a year now. Sean Purcell and I recorded a teleconference for California REALTORS about the Treasury bailout of the GSEs.

We talk about what exactly happened and what the near-term (3-4 month) effects and medium-term (12-18 month) effects on underwriting guidelines and rates. We also guessed at what the long-term (2-10 years) effect on conforming loans will be, in light of the mandate for the GSEs to reduce their portfolios.

The podcast lasts for about 15 minutes with 10 minutes of good questions and commentary by Marlene Bridges, Orange County REALTOR, Roberta Murphy, San Diego REALTOR, and John Novak, Las Vegas REALTOR. While I told the participants that their questions wouldn’t be recorded, it appears that they were. Thanks to everyone who participated in the call.

We’ll be doing more of these teleconferences on a regular basis.

That image looks nice, but I’m pretty sure it’s a mistake. We’re growing, always, but I don’t think we’re growing quite this fast.

That image looks nice, but I’m pretty sure it’s a mistake. We’re growing, always, but I don’t think we’re growing quite this fast.